Social Security Administration’s 2020 Annual Report

The Social Security Administration (SSA) has released a new report indicating that it expects the program to hit insolvency in 2034. Furthermore, Chief Actuary of the Social Security Administration, Stephen Goss believes that insolvency could occur as soon as 2023 if nothing is done to prevent a further recession or if indefinite cuts are made to payroll taxes.

Every 12 months, the SSA generates a report on the Social Security Trust, outlining its current and future financial status. The 2020 report concludes that lawmakers should take action sooner rather than later to ensure that the program can continue to pay out benefit amounts as promised through the Old-Age and Survivors Insurance Act.

Even though projections for insolvency have still remained at 2034 in comparison to their reports from the last several years, their current and future projected deficits do not include the negative impact that the COVID-19 pandemic can and will have on the Social Security Trust. Although, it wouldn’t be surprising that this pandemic could seal the fate of the future of the Social Security program as it has affected almost every aspect of society today, and there is no telling when things will return back to normal. With so many people now unemployed, it makes sense that the program is likely to take a larger than normal hit this year.

Whats-more, your monthly Social Security checks will be calculated based on the 35 highest-earning years of your career, so if you spend a significant amount of time unemployed or are forced to retire early because of COVID-19, you are lowering your earnings potential and eventual retirement payout.

And, while it is no secret that Social Security has had fiscal problems for years, if the COVID-19 pandemic results in economic losses of 15% or more for 2020, Stephen Goss, chief actuary of the SSA is quoted as saying, “…another year of loss would move the date [of insolvency] even closer.”

It is important to note that the word insolvency does not mean that the Social Security system would be bankrupt, but that they would most likely be forced to make broad mandatory cuts in benefits for all Americans receiving Social Security. By current “cut” projections, every American in 2034-2035 would begin to only receive $0.76 cents for every dollar of Social Security benefits.

Is there a solution to fix Social Security?

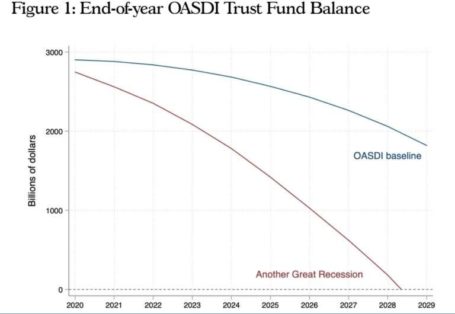

Law and policymakers must be very careful in terms of the response they take to solve the stressors that COVID-19 has put on the American financial system. A quick and un-thoughtful response could trigger a long-term recession, thus making Social Security’s situation even more urgent. For example, if a recession the same or greater than the recession experienced back in 2008 were to occur again, that could mean insolvency for the Social Security trust by the end of the decade. Congress is going to have to consider all available options, which could mean changing eligibility ages, moderating benefit growth, or increasing payroll taxes to current working Americans. Without these measures, there simply won’t be enough money left to pay 100% of the scheduled benefits to those receiving Social Security payouts.

Conservatives and Liberals have been at odds determining what the best solution may be in order to stop the bleeding from the Social Security Trust. Liberals prefer increased taxation, preferably for people who make $250,000 in income per year. Conservatives prefer decreased spending, mainly by increasing the age at which people can obtain full benefits. Their inability to come to an agreement on a solution is why Social Security has not already been fixed.

Taking matters into your own hands

This may mean that Americans will need to take their financial future into their own hands. Baby Boomers and beyond need solutions. In fact, a recent AARP Survey indicated that seniors have low confidence that savings and Social Security will cover living expenses. If you’re planning on retiring in the next decade or so, there’s a chance you’ll be receiving less than you expect from Social Security unless Congress comes up with a solution before then. That means it’s a good idea to make sure you won’t be over-relying on your benefits in retirement.

To check your current expected benefits and figure out if you should invest in something like an annuity or life insurance to bring certainty to your financial situation during retirement, Guardian Life created this worksheet to determine if your sources of income are enough to live a comfortable lifestyle during retirement.

Social Security Administration has also built a great website (my Social Security) to see personalized estimates of future benefits based on your real earnings, see your latest statement and review your earnings history.

PlanGap.com describes Plan Gap ™ Retirement Insurance and how disruptions in retirement income can be caused by many factors, but broken promises made by the government or an employer are a cause American seniors need to protect themselves against. The Plan Gap Annuity can help protect your Social Security benefits from government mandated reductions.

At the end of the day, Social Security is a critical income source for seniors. Every American deserves a thriving financial future, and if the government can’t give us our benefits as promised, we may have to take matters into our own hands to ensure a solid financial future.

Fifteen years might seem like it is far away… but it’s really not.

If you are 50 years old now, you’ll be 65 when Social Security becomes insolvent. Taking action and planning your finances now will save you from a lot of worry later on.

Kate writes about retirement benefits for retirementinsurance.org. She has a Masters Degree in Social Work (MSW). She has over a decade of experience in assisting elderly and disabled populations navigate governmental and private programs to obtain the monetary assistance they need to lead better lives. As she watched her parents begin their own retirement journeys and navigate similar systems to obtain Social Security, Medicare and other retirement benefits, she gleaned a further personal knowledge about the topic and is eager to share what she has learned with others.